Oct 25

October at a Glance: Stabilising, But Stalled

Key Insights on NZ’s Employment Market October 2025 Edition

As the year draws closer to an end, New Zealand’s economy is showing signs of balance after a turbulent period. Inflation has eased, borrowing costs have fallen, and investor confidence is beginning to return. Yet beneath the surface, the recovery remains uneven. Businesses are cautious, jobseekers are struggling, and key industries like infrastructure and construction are still waiting for stable funding. The question now is whether the country can turn this moment of stabilization into real progress, creating growth that is both sustainable and inclusive.

Middle of spring, where are we at economically?

As we move closer to the end of 2025, the feeling of hardship is being shared across nearly every sector. The state of the economy is often discussed, but what has actually changed under the current coalition, and what conclusions can we draw?

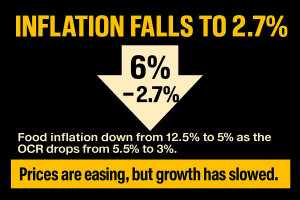

The most notable win has been the fall in inflation, dropping from 6% to 2.7%, with food inflation easing from 12.5% to 5%. Mortgage rates have also declined to around 4.9%, supported by the OCR being lowered from 5.5% to 3%. These are significant achievements and typically create the conditions for renewed growth, but they come with a catch.

Reduced economic activity has been the trade-off. As borrowing and spending slowed, businesses faced weaker sales, hiring paused, and unemployment rose to 5.2%. GDP has also contracted, showing that while prices are stabilizing, the economy itself has lost momentum.

In simple terms, New Zealand has regained price control by applying the brakes. It was a necessary correction after years of overheating, but one that has left households and businesses feeling the strain. The challenge now is to shift from cooling the economy to carefully reigniting growth without allowing inflation to surge again.

Looking ahead, most economists expect 2026 to mark the beginning of a slow recovery. Lower interest rates and strong commodity prices are likely to provide a lift, but meaningful improvement will depend on renewed investment, productivity gains, and a careful balance between spending and stability.

Real Estate, Regions and Re-Location

As the economy continues to stabilise after a difficult two years, signs of recovery are starting to appear in the property market. Real estate investment has gained momentum as inflation cools and interest rates fall, creating a more stable environment for growth. The commercial and industrial sectors have strengthened through 2025, supported by lower borrowing costs and renewed investor confidence. In Auckland, industrial properties are returning around 5.25% each year, meaning investors are seeing strong income from warehouses and logistics sites. Vacancy rates are also very low at just 2.8%, showing that almost every available space is being leased. Compared to major Australian cities like Sydney and Melbourne, Auckland’s market is performing better, with tighter supply and higher returns for investors. Analysts believe this strength will carry into 2026, driven by cheaper borrowing costs, infrastructure upgrades, and rising confidence across the sector.

That stability is also flowing into regional housing markets, which are now recovering faster than the main centres. CBRE’s latest Residential Valuer Insights survey found Southland, Canterbury, and Waikato leading the rebound, with valuers predicting price growth of up to 5% over the next 12 months. Nearly 90% of valuers identified first-home buyers as the most active group, a sign that improved affordability and lower mortgage rates, now averaging around 4.9%, are bringing more people back into the market. Meanwhile, Auckland and Wellington remain subdued, with most valuers describing demand as soft or shifting toward a buyer’s market.

These changes in both investment and housing reflect a broader shift in how people are responding to the economy. With unemployment now at 5.2% and 12.9% of young people not in education or work, the government has encouraged jobseekers to look beyond the main centres for opportunity. Prime Minister Christopher Luxon has pointed to regional industries like horticulture as being short of workers, but those on the ground say these jobs often require experience, physical fitness, and offer limited security.

While both investors and jobseekers are looking to the regions for growth, the reality is more complex. For some, it represents a chance to reset in a more affordable market. For others, the cost of relocating, limited job availability, and distance from family support make it difficult to follow opportunity. The real challenge ahead lies in ensuring regional growth is backed by sustainable employment and long-term investment, so that recovery can reach beyond the numbers and into people’s lives.

Where to From Here

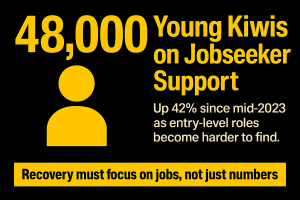

The Prime Minister says young people need to get jobs. These young New Zealanders say it isn’t that easy. More than 48,000 people aged 18 to 24 are now on Jobseeker support, up 42 percent since mid-2023, as entry-level work remains scarce. Recruiters say the number of available roles is down 50 to 70 percent across much of the country, describing the job market as the toughest since 2005. While the government points to horticulture and regional industries as options, relocation is rarely realistic when housing is limited and most seasonal jobs last only weeks.

At the same time, the industries that could create large-scale employment such as construction, infrastructure, and energy remain stalled by funding uncertainty and slow consent processes. AECOM’s 2025 Infrastructure and Buildings Survey found only one in five industry leaders have confidence in government financing, and the sector has lost up to 15 percent of its skilled workforce overseas in the past 18 months. Without a stable pipeline of projects, New Zealand risks another boom and bust cycle that limits both growth and opportunity.

The broader economy is beginning to stabilize, with inflation falling, investment picking up, and confidence slowly returning, but the benefits have yet to reach those most affected by the slowdown. If 2026 is to mark a genuine recovery, policy and investment will need to align around job creation, not just fiscal control. That means unlocking infrastructure funding, supporting skills training, and turning short-term relief into long-term employment. The challenge now is ensuring the recovery builds more than numbers, it builds futures.